JLL Update: What’s in Store for Indian Real Estate in 2019?

2018 has been a rewarding year for Indian real estate. It is, however, a result of the turbulent two-year period from 2016 to 2017 when reforms such as the RERA, demonetisation and GST were announced and implemented, and the industry remained cautious in adopting these reforms and re-calibrating business models.

In addition to these, reforms such as the Insolvency and Bankruptcy Code 2018, setting up of a dedicated Affordable Housing Fund and the government’s nod to allow 100% foreign direct investment in single brand retail under the automatic route have improved the market sentiment for both industry and investors. These reforms along with other policy measures have catapulted India’s position to the 77th rank in 2018 on the World Bank’s Ease of Doing Business 2019 Rankings from the earlier rank of 100, recorded a year ago.

The government’s focus on improving infrastructure, lowering policy hurdles to streamline project approval processes, improving ease of doing business along with rising levels of occupiers’ interest, and regular flow of capital has made Indian real estate lucrative for investments. This trend is likely to continue in 2019 as well.

JLL Research highlights some of the big trends that we see emerging across key segments and also presents a forecast for 2019:

Office segment grows strong

India’s economic growth continues to help the office market to expand further and attract more investors. With strong leasing and investments across offices, the segment remained buoyant with optimistic prospects.

India Office Market Snapshot

|

2018* (mn sq. ft.) |

% growth (Y-o-Y) |

2019** (mn sq. ft.) |

% growth (Y-o-Y) |

Net Absorption |

33.3 |

16% |

37.4 |

12% |

New completion |

38 |

41% |

43.6 |

15% |

Vacancy |

14% |

|

14% |

|

* JLL REIS Estimate **JLL REIS Forecast

The office market exhibited healthy growth of 16% in 2018 with net absorption estimated to cross 33 mn sq ft during the year. This trend is likely to continue, with net absorption expected to surpass 37 mn sq ft by the end of 2019.

Signalling good news for occupiers and investors, demand for offices remained high across key markets. The demand traction is supported by a strong supply pipeline with new completions in 2018 estimated to be at 38 mn sq ft, resulting in stable vacancy levels. The new completions are expected to further strengthen in 2019 and cross 43 mn sq ft.

Structural reforms and a refined framework for establishing Real Estate Investment Trusts (REITs) have propelled developers to build quality offices. Positive developments such as the listing of REIT by Blackstone-Embassy JV, which is likely to happen in early 2019, will open the market for similar REITs by other players.

As focus gradually shifts to the development of modern offices that meet the aspirations of new age occupiers, the market will see more such supply in the coming quarters. Hence, there will be a change in the proportion of Grade A stock in the decentralized markets. This would result in the emergence of alternate Central Business Districts (CBDs) in and around cities.

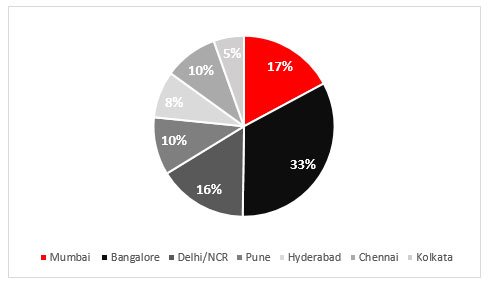

City-wise Distribution of Net Absorption in Office Segment in 2018

Bengaluru dominated the net take up in office spaces followed by Mumbai and Delhi/NCR. These three markets accounted for 66% of the demand in office spaces across the top seven cities in the country. Source: JLL REIS

Additionally, a significant change in occupier trends has been witnessed with a marked increase in the collective take up of co-working spaces. The share of co-working spaces in total office leasing increased to 10% in 2018 from 5% in 2017. With more supply likely to come in the near future, leasing activity is expected to intensify in 2019. In addition to the strong demand from start-ups and SMEs, large mainstream corporates are also actively looking at these new age office spaces.

Residential segment regains momentum

The dust over policy changes has been settling fast as developers continue to focus on delivery of existing projects. Post the slowdown in 2017, launches in the residential segment revived and are estimated to cross 175,000 (68% Y-o-Y) by the end of 2018. With the support of government incentives, developers have been able to realign themselves to tap into the opportunities available in affordable and mid-segment housing. Additionally, the commitment of USD 1.6 bn platform funds into the affordable segment indicates the growing focus of investors and developers. The trend is likely to continue in 2019, however, we expect heightened activity in affordable and mid-segment housing.

While the market has realigned itself to real demand, the transformation has helped in sales revival across most cities. As a result, residential sales volume is expected to exceed 140,000 (47% Y-o-Y) units by end of 2018. With the government’s recent proposal to rationalise GST in residential real estate, we believe the under-construction segment is going to see further traction in 2019. However, housing prices are likely to remain range-bound across most key markets.

Other than affordable and mid-segment housing, evolving segments such as student housing and co-living are increasingly attracting investors. With a millennial population of over 400 mn, these housing models hold significant potential in the Indian market.

Retail market witnesses revival

After a subdued 2016 and 2017, India’s retail market has seen a revival in 2018. In the past, growth of the retail segment had slowed due to a weak consumer and investment sentiment. However, favourable policies from the government, consolidation of large as well as small e-commerce players, technology disruption and ease of shopping, increasing consumer base, and the entry of foreign retailers have made the environment conducive for growth.

Reformative policies such as clarity in taxation through the introduction of GST, easing of entry norms for single-brand retail, rationalization and consolidation of mall space, and omni-channelling by retailers have added to the overall growth of this segment.

The retail segment is estimated to witness new completion of 3.1 mn sq ft of space during 2018. Against this, almost 3.9 mn sq ft of space is likely to be absorbed during the year. While the net absorption is expected to almost double in 2019 in comparison to 2018, new completion is likely to be over three times in the coming year. This would significantly add to the existing supply.

India Retail Market Snapshot

|

2018* (mn sq. ft.) |

2019** (mn sq. ft.) |

Net Absorption |

3.9 |

7.7 |

New completion |

3.1 |

10.2 |

Vacancy |

13.3% |

14.6% |

Note: Numbers pertain to Grade A mall space

*JLL REIS estimate; ** JLL REIS forecast

Similar to 2017, fast fashion, F&B and entertainment operators dominated leasing with superior quality malls being the main target for space in 2018. Among the three categories, F&B operators followed by apparel remained the most active category across prime high streets.

As retailers continue to focus on experiential shopping, technology interface, and e-commerce, new formats are likely to be seen in 2019. F&B, fast fashion and entertainment zone operators will continue to dominate on this front, as they did in 2018.

The year 2018 also witnessed the comeback of private equity investors in the Indian retail sector. The trend of investments that began in 2016 has continued in 2018 too with leasehold retail assets across the country being their favourite. In fact, investments in retail real estate over the last four years at USD 1.6 bn dwarfs the cumulative investments of USD 134 mn during 2009-2014.

Fully operational marquee retail assets, especially in Tier 1 and 2 cities have been on the radar of investors. In 2019, we expect investors to show further interest in ‘development assets’ (under construction, restructuring and greenfield malls). As far as the geographical spread is concerned, select Tier 2 and 3 cities are likely to emerge as the next opportunity centres.

Logistics and warehousing sector stands out

Rising levels of investments by global investors have kept the spirits high for the industrial sector. The year 2018 saw some big-ticket investments announced by ESR-Allianz tie up and HIFL (Hindustan Infralog Private Limited), a joint venture between Dubai-owned DP World and India’s National Investment and Infrastructure Fund.

While ESR-Allianz tie up has announced to invest USD 1 bn in the logistics and warehousing sector, HIPL has committed USD 3 bn to develop ports, logistics and related sub-segments.

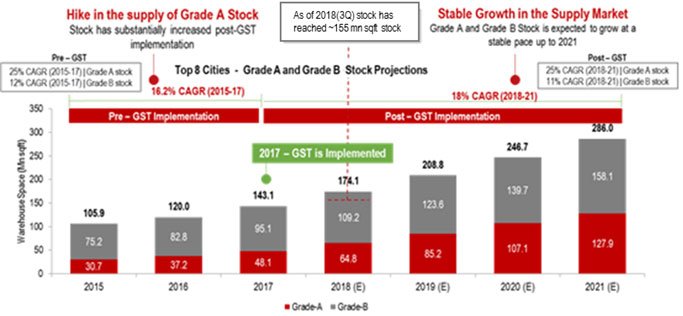

Having received the infrastructure status in late 2017, the sector has seen significant expansion in the past one year. The sector got a boost post the implementation of GST. Overall warehousing stock across top seven cities (NCR, Mumbai, Bengaluru, Chennai, Kolkata, Hyderabad and Ahmedabad) stands approximately at 174 mn sq ft in 2018.

High demand from occupiers has kept the investment sentiment high in this market. This has helped in gradual increase in supply momentum over the past one year. It is likely that higher occupier demand will continue to stimulate the supply in 2019 too. Supply pipeline remains equally robust as developers backed by the demand from large players (mostly by 3PL, e-commerce and automobile/electronics & engineering sector) that have driven leasing in the sector continue to expand and consolidate spaces in the major hubs of the country.

The investable stock (or Grade A and B) of warehousing has grown from a mere 106 mn sq ft in 2015 to 174 mn sq ft in 2018. It is expected to reach around 209 mn sq ft in 2019. Of this, Grade A spaces have grown from 30.7 mn sq ft in 2015 to 64.8 mn sq ft in 2018. The share of Grade A will increase on a regular basis and is expected to reach close to 85 mn sq ft in 2019, according to JLL estimates.

India has seen strong growth in the absorption of warehousing space and this was recorded to be slightly over 19 mn sq ft in 2017 from 10.3 mn sq ft in 2015. The first three quarters of 2018 has already seen absorption of over 17.5 mn sq ft and the year is expected to close at approximately 27 mn sq ft with majority of absorption being contributed by top eight cities.

Going forward, a key driver will be the focus of logistics and warehousing developers on increasing their footprint and supply of space in Tier 2 cities. As a result of the high demand and continuous supply, rents would remain stable in most of the markets in the short term. However, select markets which have a large supply in the pipeline may witness pressure exerted on rents with increased competition.

Post implementation of GST, the sector will continue to evolve into a mature market driven by global players with growing preference for Grade A space. The sector is expected to witness consolidation giving rise to larger tech-driven modern warehousing spaces which will bring in the required efficiency and economy of scale.

- end -

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with operations in over 80 countries and a global workforce of 88,000 as of September 30, 2018. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com